Service hotline

+86 0755-83044319

release time:2022-03-17Author source:SlkorBrowse:14253

This paper mainly introduces the MEMS sensor industry in China, discusses the difficulties and key points of MEMS replacement in China, and gives conclusions and solutions.This article has many ideas worth reading. In particular, it is pointed out that the research and development capability of companies is the key to the breakthrough of domestic substitution. Stable cooperation between enterprises and downstream manufacturers is the key to continuous product iteration. Strong capital recognition is also one of the driving forces for the rapid development of the company.

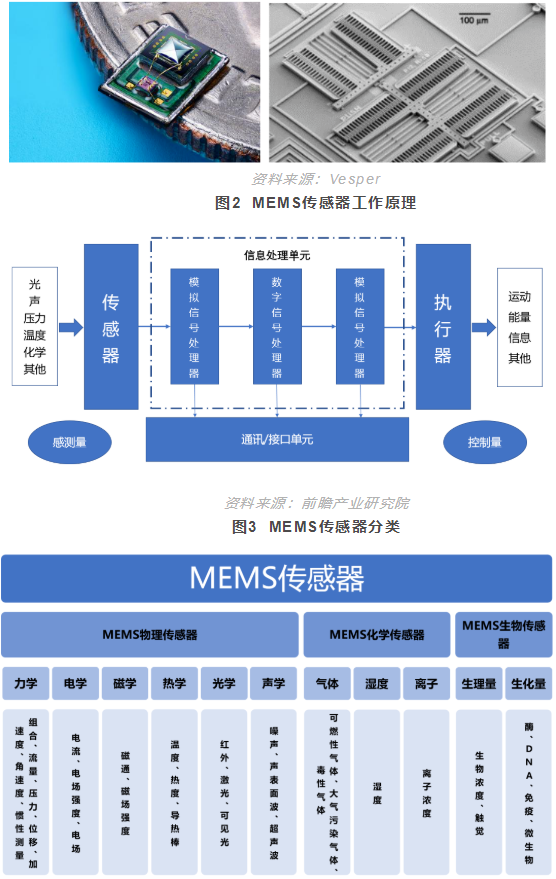

MEMS, short for Micro Electro Mechanical System, is a System that integrates microcircuits and micromachines on a chip according to functional requirements.

MEMS is based on photolithography, corrosion and other traditional semiconductor technology, integrated with ultra-precision machining, and combined with mechanics, chemistry, optics and other disciplines knowledge and technical foundation, so that a millimeter or micron MEMS has accurate and complete mechanical, chemical, optical and other characteristics of the structure.

MEMS products can be mainly divided into MEMS sensors and MEMS actuators, wherein sensors are used to detect and detect physical, chemical, biological and other phenomena and signals, and actuators are used to achieve mechanical movement, force and torque and other behaviors of devices.

FIG. 1 MEMS sensor and local micromagnification

Source: Sadie Advisors

MEMS sensor is a micro sensor manufactured by micro-electronics and micro-mechanical technology. There are a wide variety of MEMS products, and it is the most widely used MEMS products. Through the micro sensor components and transmission units, the input signal is converted and exported to another monitored signal.

Compared with the sensors manufactured by traditional technology, it has the characteristics of small size, light weight, low cost, low power consumption, high reliability, suitable for mass production, easy integration and intelligent realization.

MEMS sensors are widely used

As a key device for information acquisition and interaction, MEMS plays an important role in promoting the miniaturization of mechanical systems. MEMS sensors have been widely used in automotive electronics, consumer electronics, aerospace, biomedical, industrial and other fields.

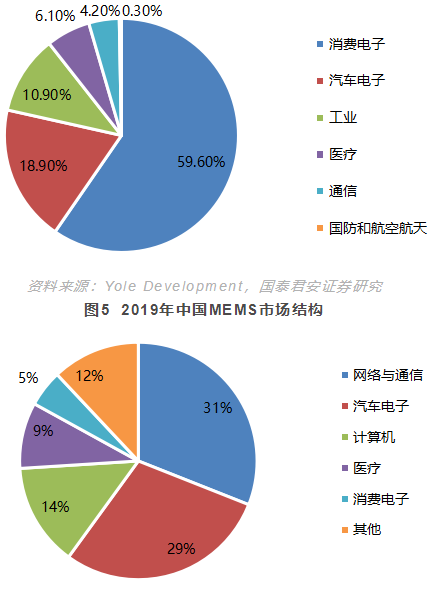

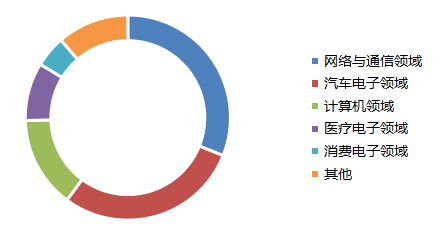

Consumer electronics and automotive are the main applications of MEMS. From the perspective of global MEMS market structure in 2019, consumer electronics is the main application field, accounting for nearly 60%; Automotive is the second largest application area, accounting for about 19%. In terms of MEMS market structure in China in 2019, networking and communications, computers, and consumer electronics together accounted for 50%, while the automotive sector accounted for 29%.

With the further improvement of the penetration rate of new energy vehicles and the development of the Internet of things, in 2019, network and communication, automotive electronics accounted for more than half of the MEMS market applications. With the arrival of 5G and intelligent network, the penetration rate of MEMS will continue to improve, and the market space in the above fields is expected to be further opened.

图4 2019年全球MEMS市场结构

Source: Yole Development, Guotai Junan Securities Research

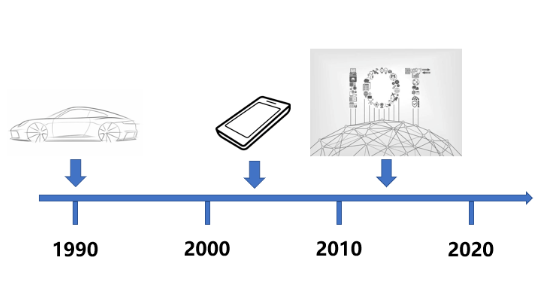

MEMS sensor development history

The first phase, from 1990 to 2000, saw the increasing use of MEMS sensors in automotive electronics and applications such as airbags, brake pressure, and tire pressure monitoring systems. This increased demand has led companies in Europe, Japan and the United States to develop and mass-produce MEMS sensors for use around cars;

The second phase, from 2000 to 2010, was driven by the rapid growth of consumer electronics. Consumer electronics such as mobile phones, tablets and laptops require MEMS sensor products to have smaller size and lower power consumption performance;

The third stage is from 2010 to 2020. With the rapid development of the Internet of Things industry, the MEMS sensor industry has a huge space for development. In addition to smart phones, tablet computers and other consumer electronics, MEMS sensors will be widely used in AR/VR, smart watches, smart driving, smart logistics, smart medical care and other fields.

The fourth stage is from 2020. With the development of autonomous driving, 5G and the popularity of the Internet of Things, the development space of MEMS is further expanded, and the performance of MEMS sensor products is improved to meet the needs of smaller, lower energy consumption and higher performance.

图6 MEMS传感器的发展阶段 资料来源:爱集微,国泰君安证券研究

资料来源:爱集微,国泰君安证券研究

The industry is just entering its growth phase

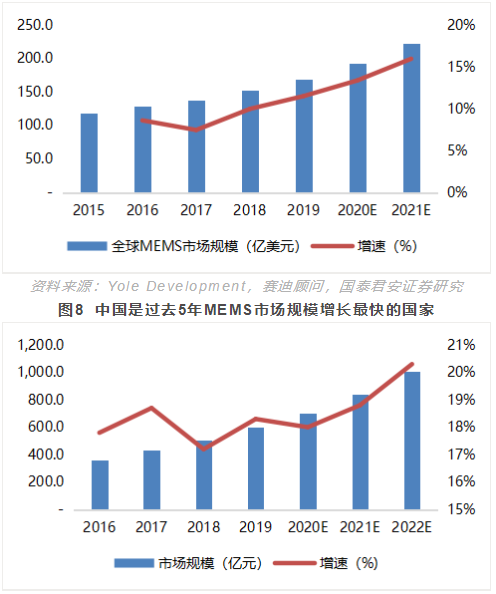

From the perspective of market size, according to Yole statistics and forecast, the global MEMS market size in 2019 was 11.5 billion DOLLARS. The growth of the market slowed down in 2020 due to COVID-19, and the market will recover from 2021, and is expected to reach nearly 17.7 billion dollars by 2025. The cagR for 2019-2025 is 7.4%.

Under the background of the rapid development of consumer electronics, automotive electronics and industry in China, China is the country with the fastest growing MEMS market size in the past five years, and is also the world's largest producer of electronic products. Mobile phones and tablets have a very large demand for MEMS products. China's mobile phone shipments rank first in the world, and suppliers of MEMS sensors such as optical sensors and motion sensors needed by the mobile phone industry have regarded China as the most important market.

According to cCID Think Tank, the size of the Chinese market was about 60 billion yuan in 2019, accounting for about 54% of the global market. The domestic market continues to grow faster than the global market, and it is estimated that the size of China's MEMS market will exceed 100 billion yuan in 2022.

Figure 7. Global MEMS market scale grows faster

Source: CCID Advisors, Guotai Junan Securities Research

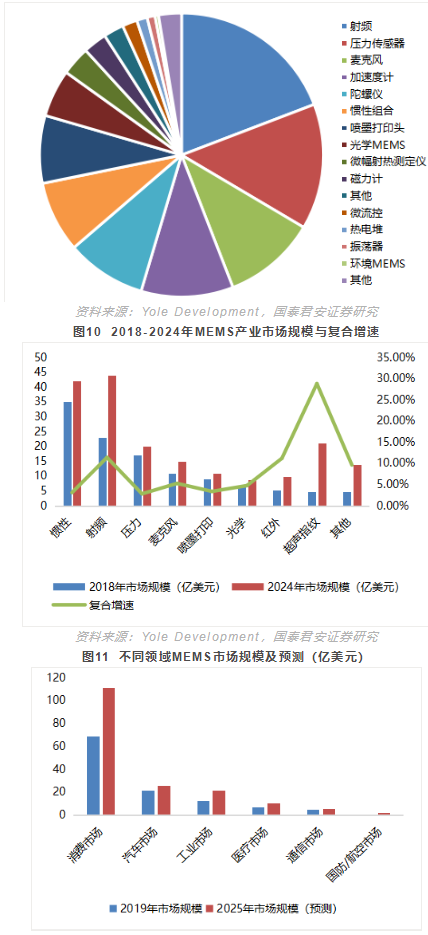

In terms of product structure, the top five MEMS sensor segments in the world are rf, pressure, microphone, accelerometer and gyroscope, accounting for nearly 65% of the total. This order for the Chinese market is rf, pressure, microphone, inertia and accelerometer, similar to the global market.

According to Yole's forecast, the $1 billion + MEMS sensor segments by 2024 include rf, inertial combination, ultrasonic fingerprinting, pressure, microphone, and inkjet printing.

图9 2019年全球MEMS市场结构(按器件类型) 资料来源:Yole Development,国泰君安证券研究

资料来源:Yole Development,国泰君安证券研究

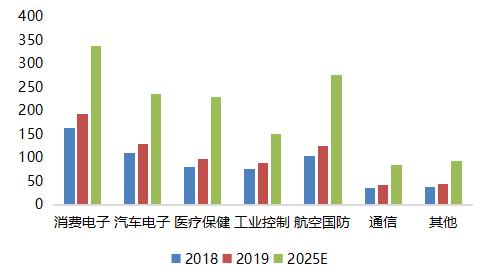

From the perspective of application terminals, driven by the Internet of Things and 5G replacement of mobile phones, the global consumer MEMS market size is expected to grow from $6.87 billion in 2019 to $11.14 billion in 2025, according to Yole's prediction. The automotive MEMS market is expected to grow from $2.18 billion in 2019 to $2.6 billion in 2025, with a 3% CAGR, driven by increased penetration of smart vehicles. In addition, the industrial, medical, communications, [敏感词] and aviation sectors of the market demand is also rising.

From the perspective of technology maturity, the development of MEMS technology in China is still in its infancy. In terms of product research and development, although the number of patent applications in China ranks third in the world, the patent quality is poor and there are few core patents. Moreover, the units applying for patents are mainly universities and research institutes, which are low in industrialization and still need to transform achievements.

In terms of packaging and manufacturing, there is a lack of OEM experience in China, and the reliability and yield of MEMS sensors manufactured by domestic OEM enterprises can not fully meet the requirements of large-scale production, and there is still a certain gap from market application.

In terms of enterprise scale, most domestic enterprises are small and medium-sized enterprises with insufficient funds and poor ability to attract talents, resulting in weak scientific research capacity and difficulty in opening channels for cooperation with universities and research institutes.

In terms of business scale and profit level, there is still an obvious gap between domestic semiconductor enterprises and foreign leading enterprises. Broadcom, an international leading company, achieved revenue of 22.597 billion US dollars in 2019, corresponding to a gross profit margin of 55.2% on sales. In 2019, STMICROELECTRONICS reported revenues of 15.416 billion US dollars and a gross margin of 38.7%. With revenue of $14.383 billion in 2019, Texas Instruments has been operating at a gross margin of more than 50 percent or even more than 60 percent in recent years.

On the other hand, in 2019, goer Shares, the top domestic enterprise, had an operating revenue of about $5.068 billion, with a gross profit rate of only 15.43%. Domestic enterprises and foreign giants contrast, revenue scale and profitability still have a big gap.

图12 部分MEMS上市公司历史毛利率(%) 资料来源:Wind,国泰君安证券研究

资料来源:Wind,国泰君安证券研究

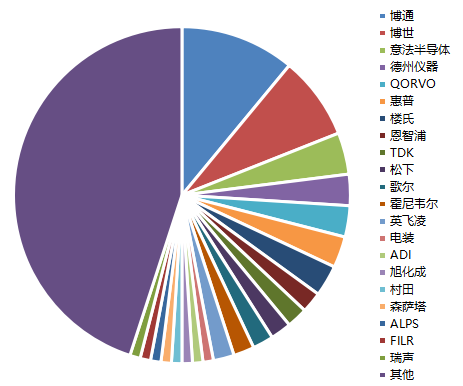

From the perspective of the number of competitors, there are many MEMS sensor types and manufacturers. In 2019, China's MEMS market is mainly dominated by foreign manufacturers, with Broadcom and Bosch neck and neck, while other major competitors include STMICROELECTRONICS, Texas Instruments, Qorvo, etc.

American manufacturers accounted for more than half, and European, American and Japanese manufacturers are relatively developed in the field of MEMS chip and MEMS manufacturing. Domestic competitors are also doing well. Goer was ranked among the top 10 global MEMS manufacturers for the first time in 2019, and Resound Technology ranked 22nd. In the foundry sector, Si Microelectronics Holdings Silex ranked first. In general, international competitors have obvious advantages, but domestic enterprises are catching up at an accelerating pace.

Figure 13 Domestic MEMS sensor industry has just entered the growth stage

Source: Guotai Junan Securities Research

In summary, based on the above analysis of market size, technology maturity, enterprise operation status, number of competitors and other aspects, we judge that the domestic replacement of MEMS sensor industry is still in the early stage of growth, and domestic MEMS enterprises are speeding up to catch up with industry giants. With the development of Internet of Things, intelligent vehicles and 5G technology, the domestic MEMS sensor industry will continue to grow, and the pace of domestic substitution is expected to accelerate.

Domestic MEMS manufacturers have great development space

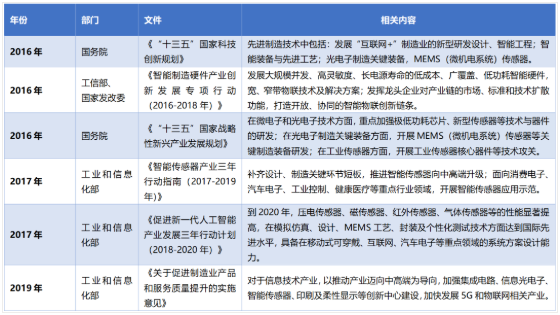

1. National policies strongly support the development of MEMS sensor industry

MEMS sensor plays a very important role in modern technology, such as Internet of Things, intelligent manufacturing, intelligent logistics and so on. China is the largest MEMS sensor market in the world, and the MEMS sensor market in China is worth paying attention to in terms of scale and importance.

The policy environment for the development of the national sensor industry continues to be optimized. With the vigorous promotion of the "Manufacturing Power Strategy" and the "Internet +" action plan, the importance of sensor technology and sensor industry will become increasingly prominent. It can be foreseen that sensor technology will be the top priority in the development of science and technology in China in the future.

表1 [敏感词]发布的部分MEMS传感器产业政策 资料来源:国务院,[敏感词]发改委,工业和信息化部,国泰君安证券

资料来源:国务院,[敏感词]发改委,工业和信息化部,国泰君安证券

2. Demand from downstream markets drives the continued growth of the MEMS industry market

The consumer electronics sector is the number one market for MEMS, thanks to the growing market for smartphones, wearables and smart homes. China, the world's largest electronics manufacturing base, consumes nearly half of the world's MEMS devices.

The continuous growth in sales of MEMS consumer electronics products in China, such as smart phones and tablets, has driven the growth of the MEMS industry, such as accelerometer sensors and microphones. In addition, with the development of intelligent driving and new energy vehicles, the MEMS market in automotive electronics is growing rapidly, with a market share of 17.8% in 2019, ranking second.

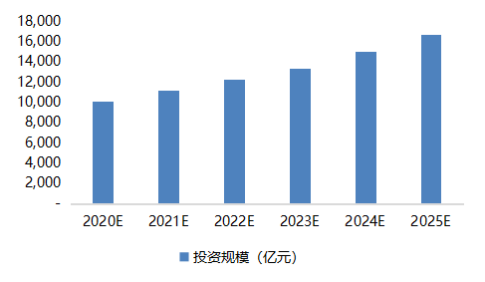

The government strongly supports the 5G sector, and China has formed a vibrant 5G industry market. Investors are full of confidence and hope in the 5G market, providing a broad space for the promotion and application of 5G.

5G is the foundation of the Internet of everything, and it also accelerates the development of the Internet of everything. The Internet of Things has become the next "tuyere" expected by all industries, and the global Internet of Things industry is developing rapidly. China's Internet of Things market is growing faster than the rest of the world and has become the most active Internet of Things application market in the world. Ccid Consultants predicts that China's 5G market will continue to grow at a high speed.

图14 中国2020-2025年中国5G投资预测 资料来源:赛迪顾问,国泰君安证券研究

资料来源:赛迪顾问,国泰君安证券研究

In the field of Internet of Things, the market is driving the rapid growth of MEMS sensor market. MEMS sensors play a key role in connecting the analog and digital worlds, and their awareness and data collection of the surrounding environment give us an objective and comprehensive understanding of the normal operation of various devices and systems.

According to the statistics of GSMA, the number of global iot devices has increased from 2 billion in 2010 to 12 billion in 2019. Benefiting from the commercialization of 5G and the development of wi-FI6, the iot market has huge potential in the future. The GSMA forecasts that global iot devices will reach 24.6 billion by 2025, with a compound growth rate of 12.7% from 2019 to 2025.

Figure 15 Rapid Growth of iot devices (unit: billion)

Source: GSMA, Guotai Junan Securities Research

In the healthcare sector, COVID-19 has brought a huge disaster to the entire world, but it has led to a huge growth in the market for medical MEMS sensors. Whether it's electronic thermometers, diagnostic devices, or ventilators, all of these medical devices are connected to MEMS sensors, leading to the rapid growth of the market in these areas.

Yole predicts that the medical MEMS market will grow by 10.6% in 2020. In addition, the epidemic has increased people's attention to health and accelerated the development of the medical consumer market. Wearable medical devices that constantly monitor physical indicators have also developed rapidly.

Due to the epidemic prevention and control, the surge in demand for contactless services, robot delivery, robot processing plants and so on has indirectly promoted the rapid development of the MEMS industry.

In addition, people's habit of automation means that even if the epidemic ends at some point in the future, people will still rely on memS-BASED unmanned, automated services, so the industry will not shrink, but continue to grow.

3. The development of domestic MEMS sensor enterprises faces certain technical challenges

China's MEMS industry started not much later than foreign countries, from the design, manufacturing and packaging three links, the existing technical conditions have initially formed a MEMS design, processing, packaging, testing of a dragon system, to ensure the further development of China's MEMS technology to provide a better platform.

However, due to the fragmentation and decentralization of power caused by historical reasons, coupled with a serious lack of investment, although many achievements have been made, there is still a big gap with foreign countries in terms of quality, performance-price ratio and commercialization.

MEMS technology research and development needs a relatively long time investment, the research and development of a sensor generally takes 6-8 years, and the time of testing and importing into the industrial chain generally takes nearly 20 years. In addition, the price of the product is not proportional to the importance of the product or the difficulty of development, resulting in Chinese MEMS enterprises can not profit from the price war.

Therefore, Chinese enterprises need to improve the supporting capacity of the industrial chain and strengthen the upstream and downstream cooperation, and actively explore the breakthrough of new materials and integration technology in MEMS devices and explore new market opportunities.

Upstream R&D and design focus on universities, research institutes and r&d pilot platform. MEMS technology involves many fields such as microelectronics, machinery, materials, chemistry, physics and so on. The interdisciplinary degree is high, the research is difficult, the design cycle is long, and it often takes several years to be able to mass production.

At present, the enterprise has certain innovation ability, but the business convergence is high, the product positioning is middle and low end, and the overall industry revenue scale is small. MEMS design belongs to the high value-added link of the industrial chain. The products of domestic enterprises are mainly mechanical sensors, which are at the middle and low-end level in the market.

In mid-stream manufacturing, the properties of basic MEMS materials, such as structural mechanical properties and material chemical properties, are the fundamental factors to determine product performance. As a result, MEMS devices rely on a variety of processes and variables, and there is often a process pipeline for each MEMS product. R&d teams typically need years of improvement and testing before commercialization.

MEMS foundry can be divided into pilot test line, IC foundry and MEMS professional foundry.

The pilot pilot line is mainly composed of universities and scientific research institutes, which serve as industrial generic technology research and development platforms, not for profit, and with limited capacity. IC OEM MEMS business is in its infancy, and its capacity is relatively weak. Most domestic design enterprises with a certain scale choose foreign OEM.

Professional OEM gradually from acquisition to self-construction, for example: at the end of 2015, the domestic manufacturer NVA acquired The Swedish MEMS OEM Silex Microsystems, thus mastering the world's leading MEMS OEM technology;

Packaging technology mostly comes from integrated circuit packaging technology, but MEMS products are more abundant, so the technology is more complex and difficult, resulting in packaging technology has become a leading field for major outsourcing semiconductor packaging test plants.

In the process of packaging and manufacturing, because China started late, and the United States, Japan, Germany and other manufacturing power manufacturing capacity and accuracy is still a certain gap, the MEMS sensor produced in life and accuracy is poor and the quality level is not uniform, the product competitiveness is low. Although domestic MEMS OEM is lagging behind the international big manufacturers, packaging and testing technology started earlier and achieved good results, and has become international competitiveness.

Among them, The main products of MEMS microphone are Goer Stock and Ruisen Technology. Because their business model is to purchase MEMS product IP from foreign design manufacturers, and then complete the packaging test and sales of products by themselves after OEM manufacturing, there is a certain premium space, and now they are in the global MEMS TOP30 camp.

In the downstream application industry, consumer electronics is the largest market, mainly due to the rapid growth of smart phones, wearable devices and other markets in recent years, and the rapid development of domestic smart device manufacturers such as China's top technology enterprise, Xiaomi and Vivo. The second is automotive electronics, automotive intelligence requires high-precision sensing equipment, such as BYD, NIO, Xiaopeng downstream domestic automobile manufacturers are also developing in full swing. In addition, medical equipment, industry 4.0, Internet of Things and other rapidly developing downstream application industries. Enterprises in the downstream of the domestic industrial chain are developing rapidly with a good momentum, but their core technologies still need foreign support and their independent research and development ability is relatively poor. Enterprises have realized the importance of independent innovation ability and continue to make efforts.

4. Capital flows to the MEMS industry have increased dramatically

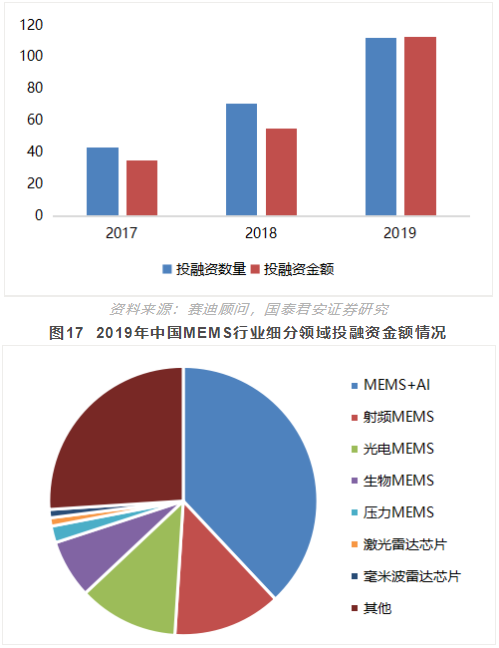

As MEMS industry is the foundation of the development of science and technology in the new era, and the policy support is strong, the investment and financing cases of MEMS industry in China are increasing year by year, both in terms of quantity and amount. In terms of amount of investment, the amount of investment in 2019 was about double that in 2018. Although the investment in the primary market was cold, investment in the MEMS industry continued to increase.

In terms of segmentation, MEMS+AI, RF MEMS, photoelectric MEMS and biological MEMS have the largest number of investment cases and amount of money. The significant increase in the number and amount of investment indicates that the capital market is paying more attention to the MEMS industry. In terms of geographical distribution, Beijing, Guangdong, Shanghai, Zhejiang and Jiangsu topped the list in terms of the number of investment cases.

图16 2017-2019年中国MEMS行业投融资情况 资料来源:赛迪顾问,国泰君安证券研究

资料来源:赛迪顾问,国泰君安证券研究

The Chinese design and OEM needs to be strengthened, and the closed test is competitive

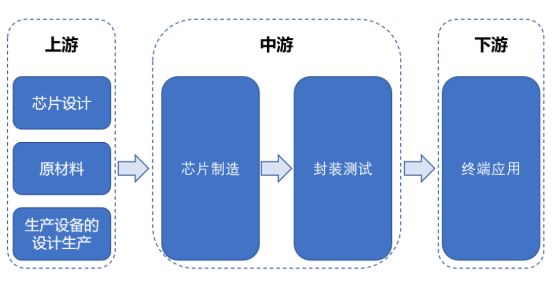

Similar to the integrated circuit industry, the MEMS industry chain mainly involves design and development, production and manufacturing, packaging and testing, and system application. The upstream of the MEMS industry chain includes MEMS device design, material and production equipment research and development and supply, the middle includes MEMS device manufacturing and packaging testing, and the downstream uses MEMS products to integrate terminal electronic products.

Upstream chip design companies focus on the design of MEMS chips and their product structure. After completing the design, they turn over to third-party fabs to produce MEMS chips. After packaging and testing, MEMS chips can be shipped to customers in consumer electronics, automotive, medical and industrial control applications. At present, MEMS manufacturing processes of domestic companies are mainly in the range of 0.25-1 micron. Manufacturing processes are not a constraint factor of the industrial chain, but function and structure are relatively more important.

图18 MEMS产业链 资料来源:国泰君安证券研究

资料来源:国泰君安证券研究

There are two modes of midstream production: Fabless and IDM. Fabless mode is the mainstream production mode at present. It is a vertical division of labor mode based on design. Enterprises are mainly responsible for the design and sales of MEMS products and outsource production, testing, packaging and other aspects. IDM mode is the integrated device manufacturing mode, which is also the main business mode of the international large factories at present. The typical IDM manufacturers are Bosch, Samsung, TI, Toshiba, ST and so on.

图19:MEMS产业链下游发展情况 资料来源:Yole Development,国泰君安证券研究

资料来源:Yole Development,国泰君安证券研究

Downstream manufacturers can be classified into two types: one is a solution provider that provides flexible customized products based on downstream requirements and then sells them to terminal manufacturers for use through simple software debugging. Second, the manufacturers that provide terminal products generally focus on specific fields, but the research and development costs are high and the research and development cycle is long. The first type of manufacturer is more suitable for products of mass consumer market, and the second type of manufacturer is more suitable for products of specialized domain.

图20 2019年中国MEMS市场应用结构(%) 资料来源:赛迪顾问,国泰君安证券研究

资料来源:赛迪顾问,国泰君安证券研究

Domestic MEMS sensor enterprise development opportunities and challenges coexist

1. Suppliers have mediocre bargaining power

MEMS upstream suppliers mainly provide raw materials, mainly silicon-based materials. MEMS materials and traditional semiconductor materials are basically the same, the supply market has been mature, the competition is more fierce, the formation of a buyer's market. When MEMS sensor suppliers face large OEM customers and OEM customers, these OEM customers rely on strong market power and demand lower price raw materials from suppliers. However, in the past two years, due to the price increase of raw materials and the limitation of wafer production capacity, the wafer link of MEMS has been restricted. The conventional 6-inch and 8-inch products are generally out of stock, and the bargaining power of suppliers has increased. It can be seen that the bargaining power of suppliers is greatly affected by market supply.

2. Buyers have high bargaining power

MEMS enterprises increase scientific research efforts, improve their respective core competitiveness, so that the rapid development of technology, product upgrading speed up, price reduction speed.

With the rapid development of the Internet of things and the accelerated upgrading of the consumer electronics market, many enterprises have joined the market and the competition has become increasingly fierce. This makes the end consumer market prices gradually reduced, manufacturers, research and development business to reduce the price; At the same time, the expansion of the end-consumption market improves the volume of end-sellers and the bargaining power of buyers.

In addition, as most domestic enterprises are good at low-end products, they also face a large number of competitors, so they need to guarantee market share through price war. It can be seen that the bargaining power of buyers is high.

3. It is difficult for new entrants to compete in existing fields

MEMS sensor industry barriers are high. First of all, there are financial barriers. Due to the non-standardized characteristics of products, MEMS enterprises cannot support a certain product through a single process. In addition to using silicon materials, there is no common basic component, which means that each MEMS product needs a different process.

However, an enterprise often needs to carry out design and development, trial processing and manufacturing, quality testing and other steps of multiple products at the same time, and there is a large capital investment. Secondly, technical barriers, MEMS design needs to cross disciplines, design is difficult. In the process of processing, each type of products need different processing technology, and each process needs the steps of process development and optimization. At the same time, due to the lack of experience in new enterprises, it is difficult to meet the accuracy and quality of processing, and the processing is difficult.

Finally, there is the talent barrier. Due to the low popularity of new enterprises and their weak ability to attract talents, it is difficult for them to surpass the existing enterprises in innovation ability and core competitiveness. However, with the continuous development of new technologies and the opening up of market segments and applications, there is a small gap between all enterprises in these fields, which provides some new enterprises with development opportunities.

4. Competition from existing competitors is fierce

Currently, American companies account for half of the domestic MEMS market share, plus European and Japanese companies, and foreign companies such as Broadcom, Bosch, STMICROELECTRONICS, and Texas Instruments occupy the majority of the domestic market. From the point of view of the main listed enterprises, there are only 2 domestic sensor enterprises with over 10 billion in revenue, which is related to the late development and competition of domestic sensor enterprises.

China's domestic supply capacity is insufficient, especially high-end products almost all rely on imported supplies, 80% of chips rely on foreign countries; The remaining share is only concentrated in the hands of a few listed companies, such as Goeracoustics, Crystal Optoelectronics, Hanwei Electronics, Shilanwei and Jinlong Electromechanical 5 companies occupy more than 40% of the domestic MEMS market; 70% of domestic MEMS enterprises are small and medium-sized enterprises, and their products are mainly concentrated in the middle and low end. In general, the current situation of Chinese enterprises is that the middle and low-end products compete fiercely, while there is no competitiveness in the high-end product competition.

5. There is little substitute threat

MEMS sensor is a substitute for traditional sensors. Compared with traditional sensors, MEMS sensor has the following advantages: miniaturization, light weight and low energy consumption. MEMS devices are small in size. Generally, the size of a single MEMS sensor is measured in millimeters or even microns. At the same time, the mechanical components after miniaturization have the advantages of small inertia, high resonance frequency, short response time and so on.

In addition, MEMS sensors are more suitable for mass production, which can greatly reduce the production cost of individual MEMS. Processing integration, a single MEMS is often in the packaging of mechanical sensors, but also integrated with other chips, convenient control of THE MEMS chip.

Intelligent sensor has information processing function, through the software can correct all kinds of errors, greatly improve the accuracy of the sensor, improve the reliability of the sensor, improve the anti-interference parts of the whole system. Under the demand of the same precision, the multi-functional intelligent sensor has significantly improved the cost performance compared with the ordinary sensor with a single function, and the multi-functional intelligent sensor can realize the measurement of multiple comprehensive parameters by multiple sensors. Combined with these advantages, alternatives to MEMS sensors pose very little threat.

Competition pattern and KSF analysis

China's MEMS market has long been dominated by foreign manufacturers, which are mature in all aspects of MEMS technology and have obvious advantages in service life and product precision.

In 2019, broadcom, Bosch, STMICROELECTRONICS, Texas Instruments, QORVO, HP, Lou, NXP, Goel and TDK ranked among the top 10 VENDORS in China's MEMS market, among which American companies accounted for 54%. Chinese company Goer made it into the top 10, and MEMS revenue grew 36% year-on-year in 2019, far outpacing other leading companies in the industry. Resound Ranked 22nd, with revenue growth of 11% year-on-year, also higher than the industry as a whole.

Figure 21. Vendor structure of MEMS market in China in 2019

Source: CCID Advisors, Guotai Junan Securities Research

At present, the overall scale of domestic MEMS sensor manufacturers is not large. In addition to The annual revenue of More than $100 million for Goer and Resound, the annual revenue of local MEMS sensor manufacturers such as Micron semiconductor, Mattel Technology, Microchip Microchip is less than $60 million, and the overall scale is small.

In addition, domestic manufacturers operate a relatively single product category, most of the product lines are one, most of them are component suppliers, and the solution supply capacity is poor. International giants Invensense, Infineon and other foreign manufacturers have 2 to 3 product lines, and Bosch, Denso, STMICROELECTRONICS and other MEMS product lines have more than 4, and they have the ability to provide integrated solutions. In contrast, it is difficult for small suppliers to achieve mass production in a short period of time, so the market share of the top big suppliers is relatively stable and the market concentration is high.

2. KSF analysis of domestic enterprises

First of all, the research and development capability of enterprises is the core of domestic alternative breakthrough. At present, the domestic RESEARCH and development of MEMS mostly lies in research institutes and universities, and the research and development capacity of enterprises is relatively poor. And the MEMS industry, as the foundation of new technology, has breakthrough new products or great improvement is an important way for it to gain a foothold in the market. Therefore, innovative and enterprises with their own core competitiveness are worthy of attention.

For example, Goer Is a leading enterprise in the field of micromicrophone; The accelerometer sensor of Suzhou Gootechnetium subsidiary ranks first in domestic sales. The gas sensor of Weisheng Technology, a subsidiary of Hanway Electronics, has achieved initial achievements and can be applied to gas detection products and smart wearable devices.

Secondly, stable cooperation between enterprises and downstream manufacturers is the key to continuous product iteration. Domestic demand is huge, excellent domestic manufacturers to cooperate with domestic large enterprises have congenital advantage, but domestic manufacturers to Fabless basic form is given priority to, compared with IDM enterprises, supply chain and distribution chain is not perfect, there is no stable, downstream vendors is a big problem, so the complete industrial chain, and large enterprises downstream enterprises with stable cooperation, As well as the existence of a long time, the system of integrity of the enterprise is also worthy of attention.

In addition, chip design and supply capacity is the basis for MEMS sensors to cope with technological iteration and innovation. Therefore, domestic semiconductor manufacturers focusing on MEMS r&d and design have broad market opportunities for import substitution and innovation.

Finally, enterprises have strong capital endorsement is also one of the driving forces for rapid development. Due to the large investment and difficulty in making profits in the initial development of MEMS enterprises, and the large amount of capital, talents and other resources needed for development, enterprises with support from large enterprises or strong investment background may develop more rapidly.

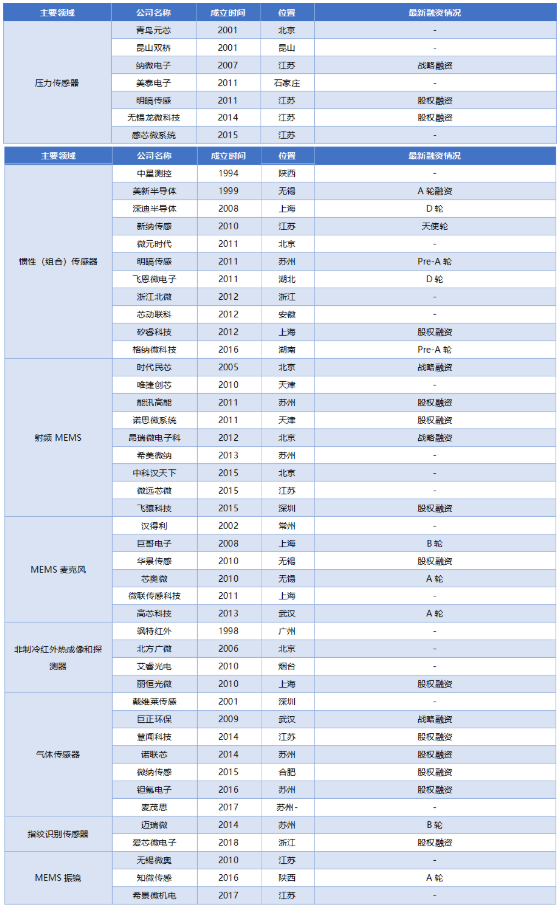

表2 MEMS非上市公司 资料来源:企名片,国泰君安证券研究

资料来源:企名片,国泰君安证券研究

The main conclusion

Main conclusion 1: MEMS sensors are rich in variety and widely used, which are the key devices to obtain information and realize interaction. With the accelerated penetration of the Internet of Things, 5G, intelligent driving and other industries, the application demand is wide and the market is huge.

According to the statistics of CCID Think Tank, the size of the Chinese market is about 60 billion yuan in 2019, accounting for about 54% of the global market, and the growth rate of the domestic market continues to be higher than that of the world. It is expected that by 2022, the size of the Chinese MEMS market will exceed 100 billion yuan, with strong domestic substitute demand. However, there is still a gap between domestic MEMS sensor product technology and performance compared with foreign giants. We judge that the MEMS industry is still in the early stage of growth.

Main conclusion 2: The driving conditions for the development of MEMS sensor industry are good, including policy support, demand growth, abundant supply, capital attention and technology iteration. However, there is still room for improvement in the process level of the industrial chain. Considering that the gross margin level of international leading companies is higher than that of domestic manufacturers, but the product pricing is higher, which gives domestic enterprises a certain space for growth. At the same time, due to the characteristics of MEMS customization, some domestic enterprises are expected to achieve technological breakthroughs in new segments.

Main conclusion 3: Compared with enterprises from developed countries, domestic manufacturers developed late and had low market share, and most of the market was occupied by American, Japanese and German manufacturers.

The local advantage is mainly in the downstream application, mode innovation and the grasp of diversified market demand. In recent years, with the application of fingerprint, image and sound sensor, enterprises with product innovation and a long time of existence are expected to gain greater space for growth, and high-quality companies are expected to emerge in all segments.

It is recommended to pay attention to mattel electronics, Deep-HAO Semiconductor, Kunshan Shuangqiao, MingHAO sensing, ENERGY hao, BIG brother electronics, Wuxi good up, Minhao Micro, micro sensors and other companies to the primary market investment opportunities.

Disclaimer: This article is reprinted from the "World Sensor Congress", this article only represents the author's personal views, does not represent the views of Sakweiwei and the industry, only reproduced and shared, support the protection of intellectual property rights, please indicate the original source and author, if there is infringement, please contact us to delete.

Site Map | 萨科微 | 金航标 | Slkor | Kinghelm

RU | FR | DE | IT | ES | PT | JA | KO | AR | TR | TH | MS | VI | MG | FA | ZH-TW | HR | BG | SD| GD | SN | SM | PS | LB | KY | KU | HAW | CO | AM | UZ | TG | SU | ST | ML | KK | NY | ZU | YO | TE | TA | SO| PA| NE | MN | MI | LA | LO | KM | KN

| JW | IG | HMN | HA | EO | CEB | BS | BN | UR | HT | KA | EU | AZ | HY | YI |MK | IS | BE | CY | GA | SW | SV | AF | FA | TR | TH | MT | HU | GL | ET | NL | DA | CS | FI | EL | HI | NO | PL | RO | CA | TL | IW | LV | ID | LT | SR | SQ | SL | UK

Copyright ©2015-2025 Shenzhen Slkor Micro Semicon Co., Ltd